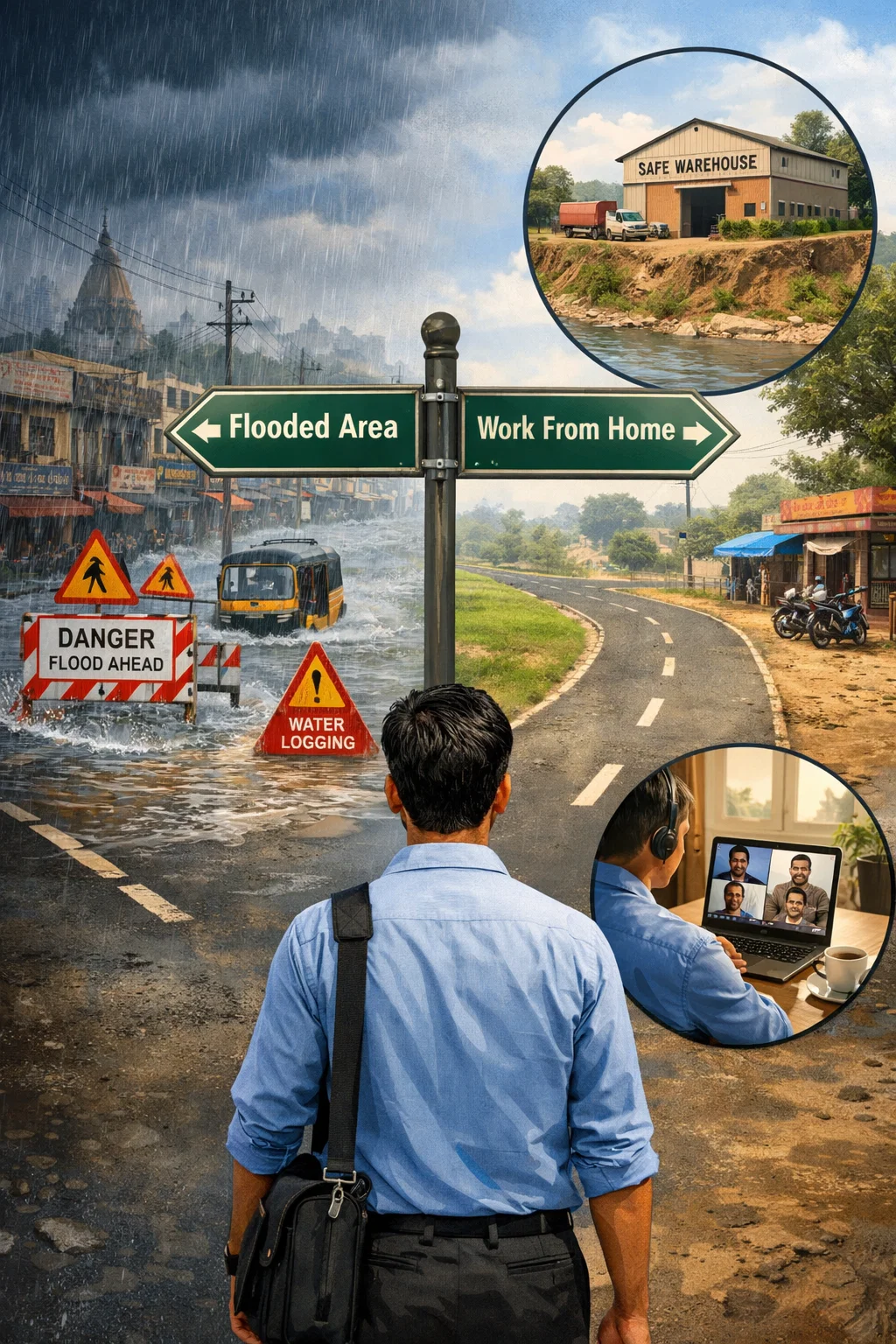

Risk avoidance is the simplest way to deal with risk: not doing the activity or staying away from the situation that creates the risk in the first place. In other words, you completely eliminate your exposure to that particular risk. The safest risk is the one you never take.

Risk prevention is about taking proactive steps to stop a loss from happening, even if you can’t (or don’t want to) completely avoid the activity. Instead of staying away from the risk altogether (risk avoidance), you reduce the chance that the risk will materialize.

In other words, you still do the activity, but you make it much safer.

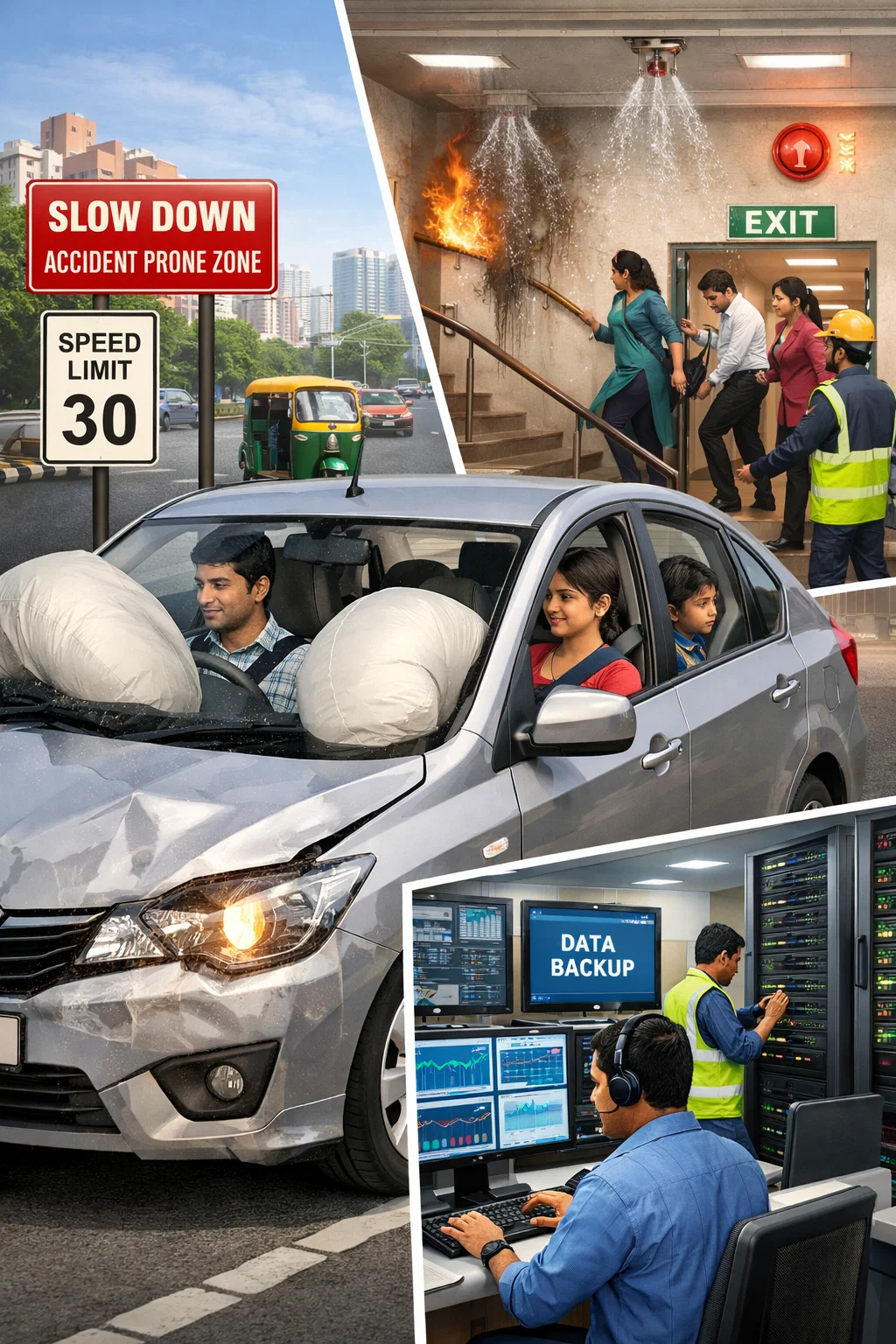

Risk reduction is about lowering either the chance of a loss happening or the size of the loss if it does happen.

Unlike risk avoidance (not doing the activity) and risk prevention (stopping the loss before it occurs), risk reduction accepts that some risk remains but works to minimize its impact. In insurance language this is sometimes called “loss prevention” or “loss reduction”.You may not remove the risk, but you can reduce the damage.

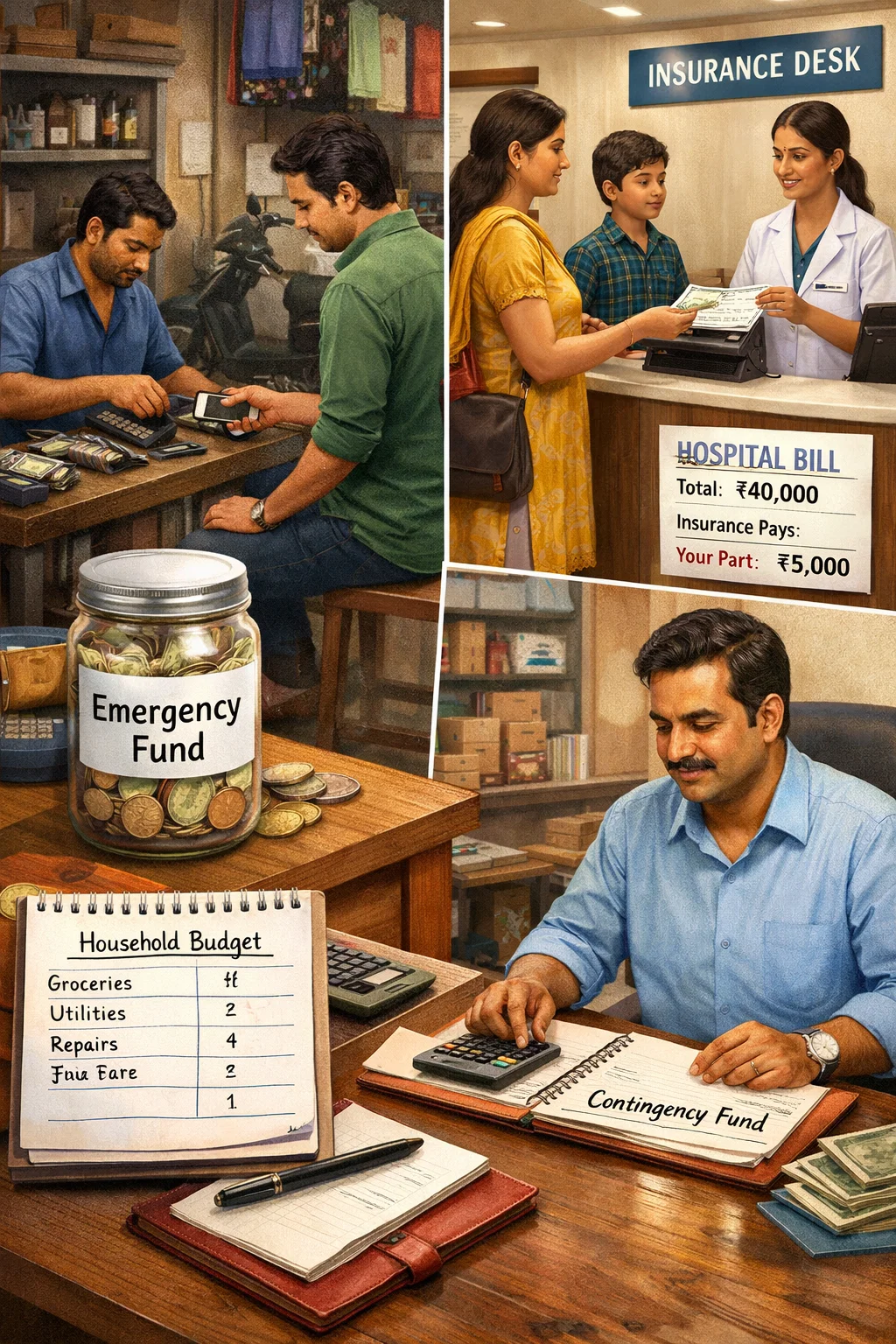

Risk transfer means shifting the financial impact of a risk to another person or organization.

You still face the event (an accident, loss or disaster may occur), but instead of you paying for the loss yourself, another party takes on that financial responsibility under an agreement.

In simple terms, “If something goes wrong, someone else will pay.”

Move the financial burden where it can be managed.

Risk retention is when you accept and keep the risk yourself instead of avoiding, reducing, or transferring it.

In other words, you decide to pay for any loss from your own money if it occurs.

It is also called “self-insurance” because you set aside funds to cover possible losses.

When you retain the risk, you fund the loss.

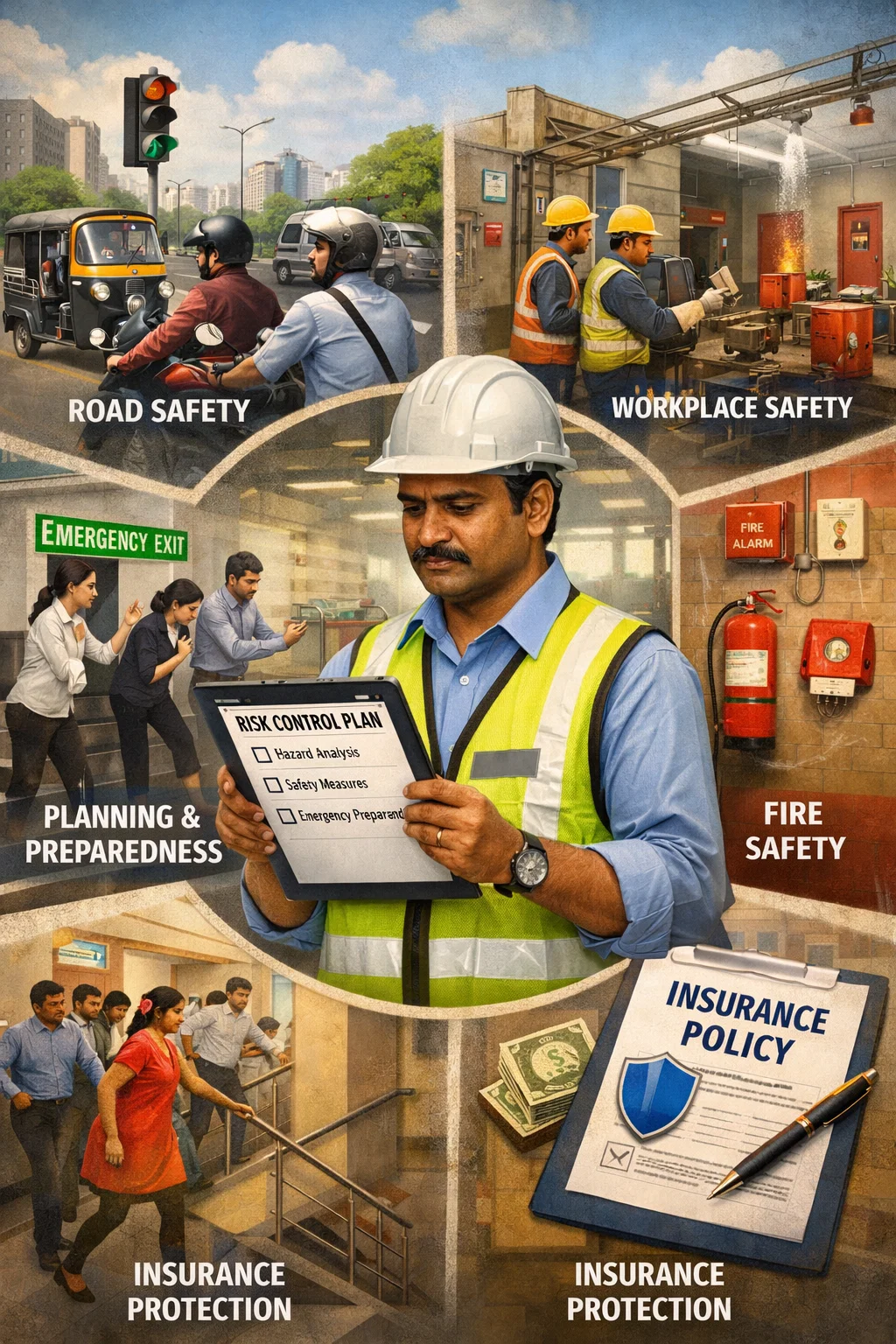

Risk control is the overall strategy of identifying, evaluating and taking actions to manage risks so that their likelihood and impact are reduced to an acceptable level.It is an umbrella concept that includes Risk Avoidance, Risk Prevention, Risk Reduction, and sometimes Risk Transfer (like insurance). Don’t avoid the activity—make it safer.

In simple words, it’s everything you do to control the causes and effects of loss before, during, and after an event.

Identify, control, and minimize the impact.